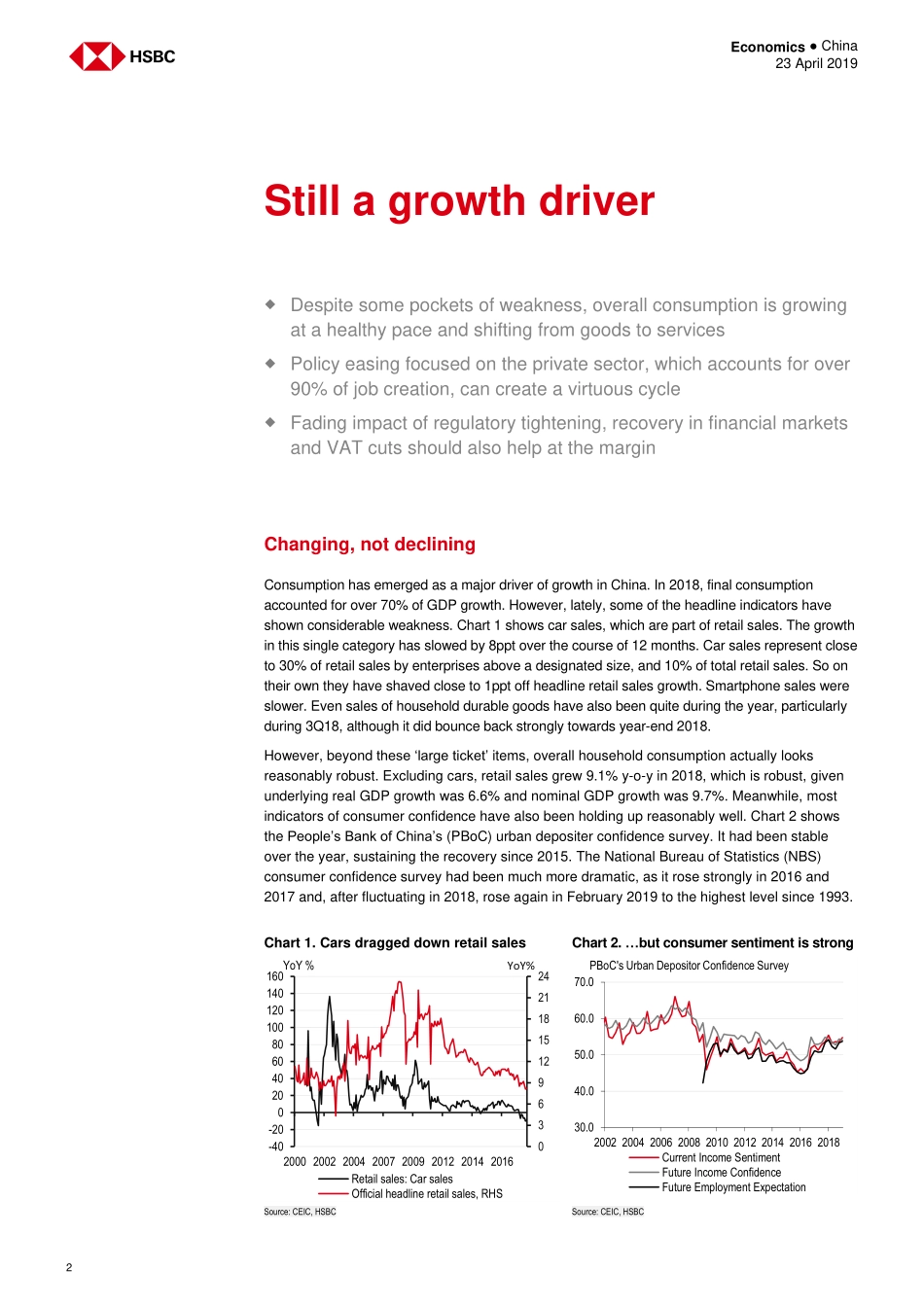

Disclosures&DisclaimerThisreportmustbereadwiththedisclosuresandtheanalystcertificationsintheDisclosureappendix,andwiththeDisclaimer,whichformspartofit.Issuerofreport:TheHongkongandShanghaiBankingCorporationLimitedViewHSBCGlobalResearchat:https://www.research.hsbc.comHSBCChinaConference201915-17May,ShenzhenRegisternowDespitesomepocketsofweakness,overallconsumptionisgrowingatahealthypaceandshiftingfromgoodstoservicesPolicyeasingthatfocusesontheprivatesector,whichaccountsforover90%ofjobcreation,cancreateavirtuouscycleVATcuts,assomearepassedontoconsumers,shouldalsohelptoincreaserealpurchasingpowerKeydriversintact:China’seconomyhasrebalancedsignificantlytowardsconsumptionoverthepastfewyears.In2018,finalconsumptionaccountedforover70%ofGDPgrowth;however,therehavealsobeenconcerns.Carsalesgrowthslowedfrom5.6%y-o-yin2017to-2.4%y-o-yin2018,shavingmorethan1pptoffheadlineretailsalesonitsown.Smartphonesalesalsoslowedasmarketleaderstookmarketshare.Yetthatwasnotthewholepicture.Othertypesofconsumption,mostlyofservices,accelerated.Andoverallurbanhouseholdconsumptiongrewahealthy9.2%y-o-y.Inourview,thestructuraldriversofconsumptioninChinaarestillintact.Thismainlyliesinthesteadyhouseholdincomegrowth,whichoverthepastdecadeshastrackednominalGDPgrowthfairlyclosely.In2018,nationalwageincomegrew8.3%y-o-y,whileurbanpercapitadisposableincome(aftertaxes)grew7.8%.Policyeasingreinforcesavirtuouscycle:Andthecurrentprivatesector-focusedpolicyeasingwilllikelyhelptosustainlabourmarketstabilityandincomegrowth.Theprivatesector(definedasnon-SOEinthisreport)isChina’slargestemployerand,overthepastfewyears,hasaccountedforalmostallofthenetincreaseinurbanjobs.Incontrast,thehousingmarketandinfrastructure,orstate-ownedenterprises(SOEs),whichhavehistoricallybeenthemainbeneficiariesofpolicyeasing,onlyaccountforanestimated19%and15%ofemployment,respectively.Inparticular,theprivatesectorisdominantinconsumer-facingmanufacturingandservicessectors,whicharewherethemajorityofjobsaregenerated.Debt,wealtheffect...